Please provide your email to download the resource

Praful Mehta, CEO of Vamstar

Report Summary

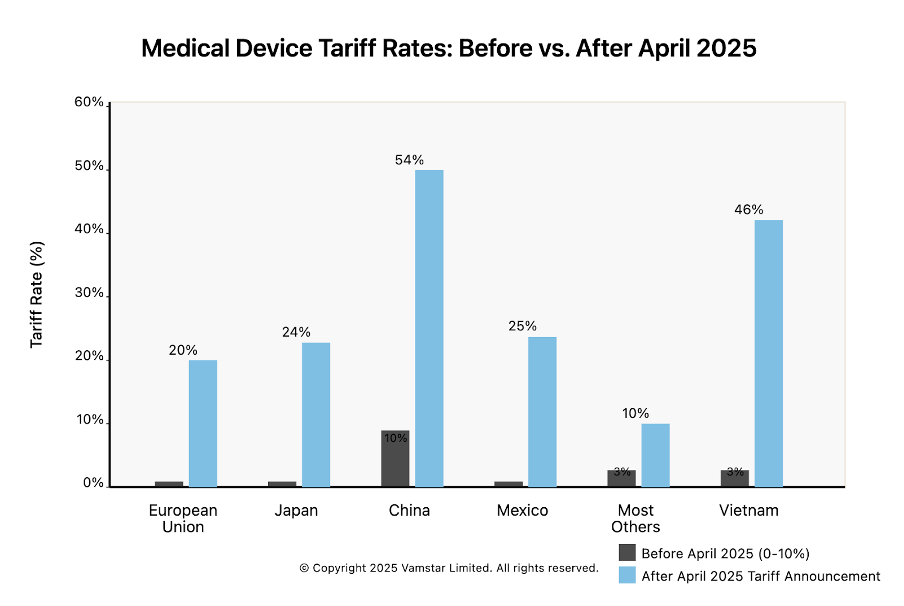

Sweeping New Tariffs on Medical Devices: On 2 April 2025, the United States announced broad new import tariffs, including a universal 10% tariff on all imports and even higher rates for certain trading partners. Medical devices, previously subject to low or zero duties, are now directly affected. For example, imports from the European Union (EU) face a 20% tariff (up from effectively 0% before), Japan 24%, China 54% (including prior trade-war duties), and Mexico 25%. These tariffs mark a stark shift from the historically low-tariff regime for medtech products.

Complex Global Supply Chains Disrupted: The medical device industry relies on an intricate global supply chain – from raw plastics, metals, and electronic components to multi-stage manufacturing, assembly, sterilisation, and packaging across continents. These new tariffs introduce friction and cost at each stage. Cross-border value chains that once optimised cost and efficiency now face tariff “taxation” at points of import, impacting both US and European companies. Tariffs act as an extra cost on imported raw materials and components, raising production costs and complicating logistics.

Differing Impacts: United States vs Europe: American and European medical device firms are affected in distinct ways. U.S. companies that import key inputs (specialty metals, electronics, sub-assemblies) see higher input costs, potentially reducing margins or forcing price hikes in their home market. However, they could gain some competitive edge within the U.S. if foreign rivals’ finished products become pricier due to tariffs. European companies exporting to the U.S. now face a 20% cost hurdle, squeezing their competitiveness in the crucial American market. Many may need to localise production to the U.S. or absorb/pass on costs. Europe’s domestic market is not directly hit by these U.S. tariffs, but European firms could become collateral damage if the EU retaliates with tariffs on U.S. medical devices. Both multinationals and SMEs are exposed – though larger firms have more flexibility to adapt supply chains than smaller ones.

Supply Chain Stage Vulnerabilities: Raw material sourcing is a first pressure point – tariffs on imported steel, aluminium, polymers, and electronic parts raise input costs for device manufacturing. Manufacturing and assembly often occur in low-cost countries (e.g. Mexico, Ireland, Costa Rica, China) to serve global markets; tariffs now penalise those cross-border production models. Sterilisation and packaging processes, if done across borders, also incur added costs. Networks that move finished devices internationally (often by shipping products from central manufacturing hubs to regional distribution centres) now face higher landed costs at borders, disrupting established distribution cost models.

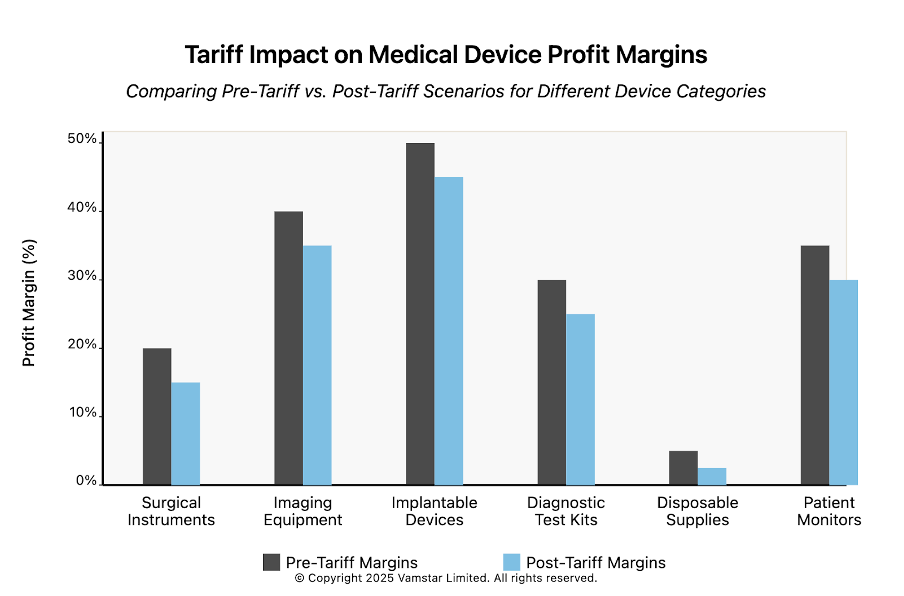

P&L and Pricing Implications: The new tariffs act like an excise tax on the medtech sector, forcing tough choices on pricing and profitability. Companies may have to raise device prices (impacting hospitals and patients) or absorb the tariff hit by accepting lower margins. For example, a device imported from Europe that previously had a 20% profit margin would see that margin wiped out by a 20% import tariff if prices remain constant. Our analysis shows tariff rates under the new regime far exceed the old – with China and Mexico facing particularly steep increases (see Figure 2). This threatens R&D budgets and could slow innovation as firms tighten spending. Hospitals, which spend ~10.5% of their budgets on medical supplies, may see cost increases propagate through the healthcare system.

Strategies and Scenarios: Companies with distributed manufacturing footprints (plants in both U.S. and Europe or Asia) are re-evaluating their supply chain strategy. Some are shifting production for the U.S. market into U.S. facilities to bypass tariffs, while using European plants to serve Europe – essentially a regionalisation of manufacturing. Others may increase inventory or use bonded warehouses and duty drawback schemes to mitigate costs. However, such adjustments take time and capital. SMEs, often reliant on single production face hard decisions as their flexibility is limited, the tariffs encourage a move toward a more localized supply chain to increase the efficiency of global networks.

High-Impact Device Categories: Certain device segments are especially affected. Surgical instruments (largely metal-intensive, with many imported from Asia or Europe) now carry higher costs due to both metal tariffs and finished goods tariffs. Imaging equipment (MRI, CT machines, etc., often made by European or Japanese firms) faces steep U.S. import duties, raising prices for U.S. hospitals or pressuring suppliers like Siemens and Philips to shift more production stateside. Disposable medical supplies (gloves, gowns, syringes) largely sourced from China and Southeast Asia, were already subject to tariffs and now face even higher rates, risking shortages or price spikes in critical items. Implants and medical electronics are caught in the tariffs on raw inputs (e.g. titanium from abroad, semiconductors from Asia), potentially increasing costs for life-saving implantables and diagnostic devices.

Outlook: In sum, the April 2025 tariffs present a significant headwind for the medical device industry’s global supply chain model. This white paper maps out the supply chain stages and analyses how these new trade barriers alter the landscape in the U.S. versus Europe. A “wait and see” approach is risky – early adaptation and strategic supply chain management will be key. Companies that proactively realign sourcing and production, negotiate with suppliers, and engage policymakers (as industry groups like AdvaMed and MedTech Europe are doing) will be better positioned to weather the changes. The following sections provide a detailed breakdown and analysis.

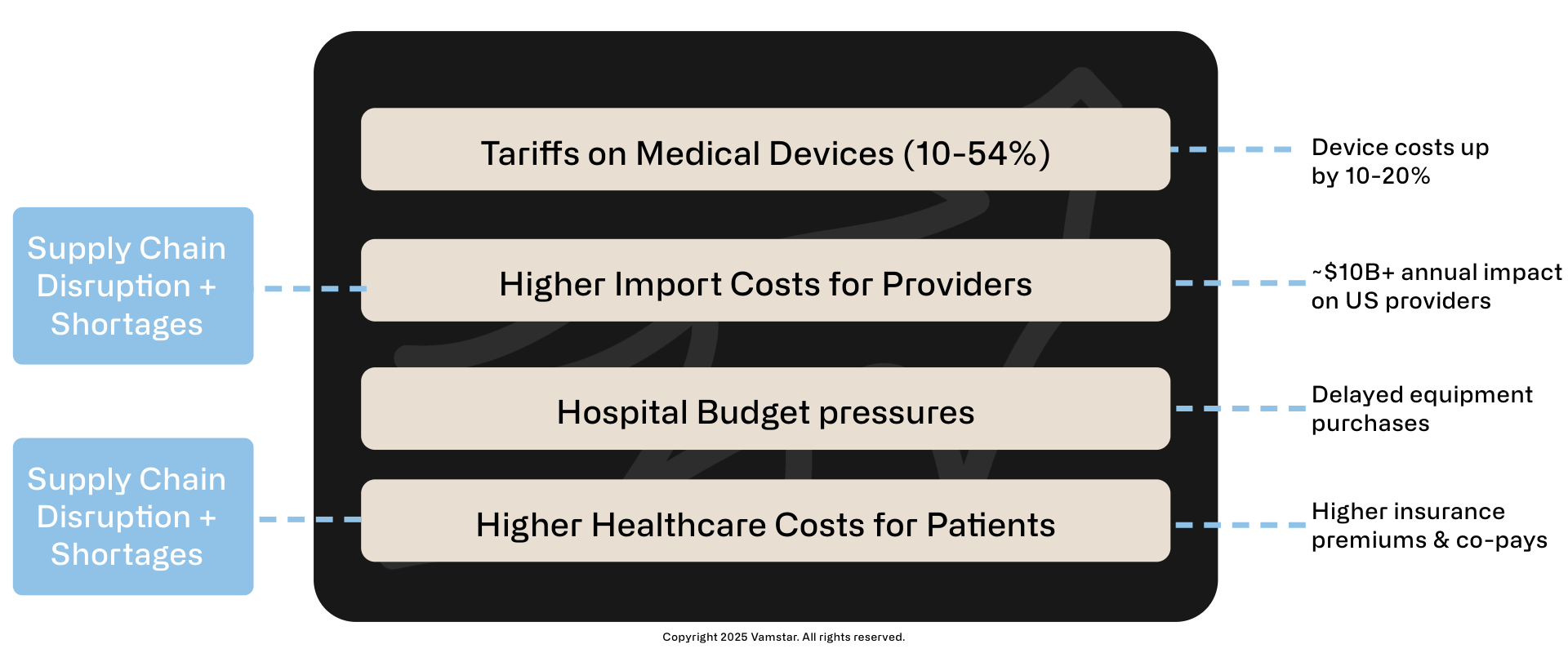

April 2025 Tariff Impact on Healthcare Costs

Cascading effect of medical devices tariffs

Figure 1: Impact of Tariff on Healthcare Costs

Key Impacts

- US Hospital expenditures on medical supplies ~ $10-20B annually (2023)

- Est. 10-20% tariff impact on imports: ~$10-20B annually

- Potential long-term impact: Slower innovation, delayed care improvements

Introduction

The U.S. Administration’s tariff announcement on 2 April 2025 represents a watershed moment for global trade in medical technology. In a Rose Garden ceremony heralded as “Liberation Day”, President Trump unveiled a sweeping new tariff plan that fundamentally shifts how imported goods – including medical devices – are treated. All imports into the U.S. now face a baseline 10% duty, with certain countries’ goods taxed at significantly higher rates. This is a stark departure from the past. Historically, medical devices and supplies enjoyed minimal tariffs as they were considered humanitarian or essential products; major trading partners kept medtech duties at no-to-low levels. Prior to 2025, roughly half of U.S. imports of critical medical products faced zero tariffs, and most others only a few percent. Now, that landscape has changed overnight.

This introduction sets the stage for an in-depth analysis of how these new U.S. tariffs – effective from April 2025 – impact the medical devices industry’s global supply chain. We will compare conditions before vs. after the tariff change, and distinguish the effects on stakeholders in the United States and Europe. The aim of this white paper is to provide strategic insights into supply chain mapping, cost implications, and potential adaptive strategies.

Tariffs announced

The key elements of the April 2025 U.S. tariff package are:

- Universal 10% import tariff: An across-the-board duty on all imports into the United States, ending any duty-free treatment for medical devices from any country.

- Reciprocal tariffs for “bad actors”: Higher tariffs on countries deemed to have unfair trade practices. The EU faces a 20% tariff; Japan 24%; and China a punitive total of 54% (a new 34% on top of existing tariffs) on their exports to the U.S. Notably, Canada and Mexico, while “excluded” from the reciprocal scheme, are separately hit with 25% tariffs on most of their imports due to other disputes.

- Pharma carve-outs: Pharmaceuticals were largely exempted or delayed in this round (following heavy lobbying), meaning drug imports avoid immediate tariffs. However, medical devices and equipment have no such exemption – a point of great concern for industry groups. AdvaMed (the Advanced Medical Technology Association) openly criticised the broad tariffs, likening them to an excise tax on medtech that will “increase overall costs to the health care system” and stifle innovation.

These measures come on the heels of an already evolving trade environment. The years 2018–2024 saw targeted tariffs under Section 301 (chiefly on Chinese goods), Section 232 (steel/aluminium), and assorted trade disputes, but medical devices were often spared the worst. Many critical medical products from China were granted exclusions during COVID-19 due to public health needs. By 2024, the U.S. still had $5 billion worth of medical goods from China under tariff (approx. 26% of all U.S. medical imports), but allies like the EU enjoyed free trade in most medtech categories. That era has abruptly ended with the new blanket tariffs.

Industry significance: The medical device sector is globally integrated and innovation-driven. From large multinational corporations to specialised small and mid-sized enterprises (SMEs), companies source materials and components worldwide to produce everything from simple surgical gloves to advanced MRI scanners. The U.S. and Europe are deeply interconnected in this trade. For instance, Europe’s top import supplier for medical devices is the United States (accounting for ~45% of Europe’s medtech import value in recent years), and the U.S. similarly relies on European and other foreign suppliers for many medical technologies. This interdependence means trade barriers can reverberate widely, affecting patient care, costs, and industry competitiveness on both sides of the Atlantic.

This industry report proceeds with a detailed mapping of the medical device supply chain, followed by the previous tariff regime versus the new April 2025 tariffs. We then assess impacts on U.S. companies and European companies, including distinctions between multinationals and SMEs. We then explore scenario analyses for companies with manufacturing in multiple regions and how tariffs apply based on production origin/destination. We then analyse implications for cost structures, profitability, and competitiveness. Finally, in the last section, we highlight specific device categories (surgical instruments, diagnostic imaging equipment, implants, disposables, etc.) that are disproportionately impacted by the tariffs, before concluding with strategic considerations moving forward.

By examining both the U.S. and European perspectives, we aim to illuminate how the same set of U.S. trade policies can have divergent consequences across geographies and business contexts.

Figure 2: Tariff Rates on Medical Device Imports into the U.S. – Previous vs. April 2025 regime.

Mapping the Medical Device Supply Chain (Raw Materials to Distribution)

The first step in our analysis is to map out a typical supply chain for medical devices, from raw material sourcing through to end-market distribution. This serves as a foundation for understanding where tariffs bite and how disruptions propagate. The medical device supply chain is often described as complex, global, and highly regulated. It involves a sequence of stages – each of which may span multiple countries and companies – 1. Raw Materials: The origin of inputs like plastics, metals, and electronics. 2. Component Manufacturing – Turn materials into parts or sub-assemblies. 3. Device Assembly – Putting together components into finished medical devices. 4. Sterilisation makes products sterile (for those that require it) using processes like ethylene oxide or gamma irradiation. 5. Packaging – Sealing and protecting the device, often with specific materials and labelling (including regulatory labels, instructions). 6. Distribution – Transporting the final packaged devices to where they are needed: hospitals, clinics, distributors, or end-users around the world.

Each stage is governed by strict quality and regulatory standards (e.g. ISO 13485, FDA QSR), adding complexity because supply chain partners must be qualified and compliant. Companies manage these steps with a mix of in-house operations and outsourcing to specialised suppliers or service providers. Figure 2 below conceptually illustrates these stages and typical cross-border flows involved:

EU/US Import/Export Dynamics

Impact of April 2025 Tariffs on Medical Device industry

Figure 3: Matrix of Dependencies and Relative Positioning

Stage 1: Raw Material Sourcing

Medical devices begin with raw materials – the foundational inputs. The main categories include:

- Plastics used in disposables (syringes, tubing, IV bags), casings for equipment, implants (e.g. PE for orthopaedic implants), etc. Sources: petroleum-derived resins from chemical companies globally (USA, Europe, Middle East, Asia). Some specialty polymers (like bio-compatible plastics or silicone rubber) may be produced in limited locations. Example: Polypropylene for syringes might be sourced from a petrochemical plant in Asia, then shipped to a molding factory elsewhere.

- Metals and Alloys: Critical for surgical instruments (stainless steel), implants (titanium, cobalt-chrome alloys), device machinery (aluminium frames, electronic contacts gold), etc. Sources: metals are mined and refined worldwide – steel may come from Europe or China, titanium often from Japan or Russia (pre-2022, with recent shifts), and rare earth metals (for electronics, magnets in MRI machines) heavily from China. The global nature of metals is notable; even if final instrument making is in Germany or the US, the raw steel might be imported from abroad.

- Electronics and Semiconductors: Modern devices (monitors, MRI, infusion pumps, pacemakers) rely on electronic components – chips, sensors, circuit boards, batteries. Sources: a global electronics supply chain with hubs in East Asia (China, Taiwan, South Korea, Japan) for semiconductors and components. For instance, a patient monitor might use a Taiwanese microprocessor, sensors from Germany, and a display from South Korea. These parts often travel to the device assembly location later.

- Textiles and Others: Some devices involve textile components (e.g. surgical gowns, wound dressings) – often sourced from cotton or synthetic fibres produced in Asia. Chemicals and reagents for diagnostic devices (like test strips) might also be considered raw inputs, sourced globally.

Before the tariffs, companies optimised sourcing based on cost and quality, often buying from the most competitive suppliers. U.S. device makers might import precision steel tubing from Germany or electronic sensors from China with negligible duties. Now, with the U.S. imposing 10% on all imports (and higher on some nations), these raw material imports have become more expensive.

For example:

- A U.S. catheter manufacturer importing plastic pellets or resin from abroad will pay 10% duty on that material.

- If those pellets come from an EU supplier, the duty is 20%. If from China, effectively 54% (since many chemicals were on prior tariff lists).

- Metals from Europe now have a 20% tariff; from Japan 24%; from elsewhere at least 10%. (Steel and aluminium were already subject to 25%/10% under earlier policies, but some allied countries had exemptions – now largely overridden or supplemented by the new regime.)

For European manufacturers, raw material sourcing is unchanged unless their materials come from the U.S. and the EU retaliates. As of early 2025, the EU was considering counter-tariffs. MedTech Europe (the European medtech trade association) urged the EU to exclude medical technologies and inputs from any retaliatory tariffs citing the risk to patient care. They noted that including raw materials, components or devices in the EU’s countermeasure list would increase costs and delay patient access in Europe. Indeed, the European Commission’s proposed retaliation list at that time did include some medical product codes, a point of contention. Thus, European companies could face tariffs on U.S.-sourced raw materials if the trade war escalates, but currently they face mainly the cost of U.S. tariffs when exporting to the U.S. (discussed later).

In summary, raw material sourcing is now a costlier and more complex stage for U.S.-bound supply chains. Companies will look towards switching source countries not heavily tariffed. However, given the breadth of the “all imports” tariff, few alternatives exist that are completely tariff-free (e.g. sourcing within the U.S. itself, which might not be feasible for certain materials or could be higher base cost even after avoiding tariff).

Stage 2: Component Manufacturing

Raw materials are transformed into components or sub-assemblies used in final medical devices. This stage often involves multiple specialised suppliers:

- Moulded Plastic Components: Factories (often in Asia or Mexico) injection-mould plastic parts like syringe barrels, catheter connectors, casing for devices, etc.

- Machined or Forged Metal Parts: Surgical instrument blanks, orthopedic implant blanks, precision machined parts (gears for hospital beds, robot surgery arms) could be made in countries with strong machining industries (Germany, Switzerland, Japan) or low-cost locations (Pakistan is known for basic surgical instruments, Costa Rica and Malaysia for various components).

- Electronic Sub-assemblies: Printed Circuit Boards (PCBs) assembly, sensor modules, displays – frequently done in China, Taiwan, Malaysia, etc., where electronics supply chains cluster. Even U.S. or EU medtech firms commonly outsource PCB assembly to Asia, then import the boards for final device assembly.

At this component stage, supply chains tend to be multi-tier. For example, a U.S. ventilator might contain a motor sourced from Switzerland, circuit boards assembled in China (with chips from Taiwan), and a plastic housing made in Mexico. The components come together in the final assembly stage. Each cross-border movement now potentially incurs tariffs:

- Importing components into the U.S. for assembly: now faces at least 10% tariff. If those components come from the EU or Japan, 20–24%. If from China, 54%. Even intra-company transfers (e.g. a company’s own plant in Ireland sending parts to its U.S. plant) face these duties upon U.S. entry.

- Some companies might try to perform more component manufacturing domestically to avoid this. However, building new local supplier capacity is time-consuming, and for highly specialised parts (like a MEMS pressure sensor), U.S. or European medtech firms often rely on a handful of global suppliers.

Mexico and other low-cost hubs are particularly impacted here. Mexico is a major component and device manufacturing hub for the U.S. market. Under NAFTA/USMCA, components could flow tariff-free between the U.S., Mexico, and Canada, enabling an integrated North American supply chain. For instance, U.S.-made medical device components could be sent to Mexico for assembly, then re-imported as finished devices duty-free. In fact, 92% of medical devices manufactured in Mexico are exported to the U.S., representing many billions in trade. Now, however, the U.S. has imposed a 25% tariff on most imports from Mexico. This is effectively undoing the duty-free advantage. A company that used to ship components to its maquiladora in Tijuana and bring back finished devices with zero tariff now faces a 25% tariff on the re-imported goods (unless specific exclusions or workarounds apply). That could be devastating to the cost model – Mexico offered ~25% cost savings vs U.S. manufacturing, which is entirely erased if a 25% tax is applied on return. We will explore this further in the scenarios section.

For European supply chains, component manufacturing may be less offshored than U.S. (European firms often manufacture within Europe for high-value devices, though they also use low-cost locations like Tunisia or Asia for simpler parts). A European company importing components from China was already paying EU tariffs (which are relatively low, often around 2–5% for tech components). They are not directly affected by the U.S. tariff, except if those components were going into devices destined for the U.S. market (in which case, once the final device goes to the U.S., it’s hit with tariff). European companies importing U.S.-made components might become subject to EU retaliation tariffs if enacted, but that remains speculative.

In essence, at the component stage:

- U.S. importers (including U.S. subsidiaries of EU companies) see immediate cost increases for foreign-made components.

- Manufacturers in tariff-targeted countries (like China, which now faces 54% U.S. tariff) may lose business as U.S. firms seek alternate sourcing. Indeed, even before this, many suppliers were shifting production from China to Vietnam, Thailand, or Mexico to escape earlier 25% tariffs. The new tariffs extend that pressure to those countries as well (Vietnam faces a hefty 46% U.S. tariff on goods under the “reciprocal” scheme, as an example). The “tariff whack-a-mole” could push component sourcing to countries not singled out (perhaps India or Malaysia, at 10% baseline).

- European-bound supply chains are less disrupted at the component stage, except for global price or availability effects. For instance, if U.S. tariffs make Chinese electronic parts unsellable in the U.S., Chinese suppliers might pivot to other markets, potentially affecting supply/demand and prices in Europe (perhaps glut, lowering some costs, or shortages if some suppliers fold due to lost U.S. volume).

Stage 3: Device Assembly

This is the stage where all the parts come together into a final medical device. Assembly can range from simple (screwing together a few components) to very complex (cleanroom assembly of stents or catheters, extensive testing and calibration for imaging machines). Assembly locations are a strategic choice: many companies historically assembled devices in a location optimised for a combination of cost, skill, and market proximity:

- United States: High-end and large equipment (e.g., CT scanners) often assembled in the U.S. if the U.S. is a major market – it also helps with FDA inspections and having R&D and manufacturing co-located for complex tech. However, U.S. labour costs are high, so for simpler mass-produced devices, U.S. firms often did final assembly abroad.

- Europe (Ireland, Germany, etc.): Ireland is a known hub for assembling finished devices (especially for U.S. multinationals) due to its skilled workforce and tax advantages. Germany and Switzerland focus on precision devices (e.g., endoscopes, implants).

- Mexico, Costa Rica, Puerto Rico: Popular for U.S. firms – lower labour cost but relatively close and in similar time zones. Prior to 2025, duty-free access made Mexico and Costa Rica very attractive for final assembly for U.S. consumption.

- China and Southeast Asia: Some final assembly, especially of electronic medical devices and inexpensive consumer medical products (blood pressure monitors, glucometers) was in China, though concerns about tariffs and IP led some companies to avoid final assembly in China even before 2025. Southeast Asia (Malaysia, Vietnam) captured some of this work as China became costlier in trade war years.

With the new tariffs, the location of final assembly has huge tariff implications for selling into the U.S. market:

- If final assembly is outside the U.S., importing the finished device now incurs at least 10% tariff, up to 54% from China, 20% from EU, etc. This is a direct hit when the product crosses the U.S. border.

- If final assembly is within the U.S., no import tariff on the finished device sold domestically – though remember, if the components were imported, those components paid tariffs earlier. Some companies might opt to do final assembly in the U.S. to transform the country-of-origin and reduce the tariff rate. For example, a European company could ship sub-assemblies to its U.S. subsidiary, do the last assembly steps there, and label the product “Made in USA” (if it meets the rules of origin criteria). While the sub-assemblies would have paid import tariffs, the value added in the U.S. might allow the final product to count as U.S.-made, avoiding the higher finished-good tariff. This tactic, however, only mitigates if the tariff on components is lower than on the finished product (with a flat 10% baseline, it might not matter unless escaping the reciprocal 20% by doing so).

- U.S. multinationals with dual manufacturing sites (one in U.S., one in EU/Asia) may reallocate production. For instance, a firm might decide that all production for U.S. customers will be done in its U.S. plant (even if that means higher production cost, it avoids the tariff), and the EU plant will serve EU and other global markets. Essentially, a shift from a global factory model to a regionalised model. This reduces cross-border shipments (thus tariffs) but at a cost of lost economies of scale.

European companies face a tough choice for assembly of goods destined to the U.S.: maintain European assembly and accept a 20% tariff on export, or invest in U.S. assembly operations. Many large European medtechs (e.g. Siemens Healthineers, Philips, Getinge) already have some U.S. assembly operations, but perhaps not for all product lines. They may accelerate plans to expand U.S. manufacturing footprints to sidestep tariffs. SMEs in Europe, however, might not have the resources to set up a U.S. plant; they could turn to contract manufacturers in the U.S. or partnerships, or unfortunately scale back exports to the U.S. if it’s unviable.

From the U.S. perspective, domestic SMEs that rely on importing finished devices for resale are directly squeezed. For example, a small U.S. distributor that imports niche surgical instruments from Germany will now pay 20% more for those products. They might try to pass that cost to hospitals, but hospitals have budgets and competing suppliers. The alternative is to find a U.S.-made source (which may not exist for that niche instrument, or might be an inferior product). We will delve more into the business impacts later, but it’s clear that final assembly location is now a critical factor in supply chain planning.

Another consideration at the assembly stage is compliance and regulatory alignment. Some companies historically concentrated assembly in one site per product to streamline quality control and regulatory filings. Having duplicate production lines (one in EU, one in U.S.) means duplicate FDA and EU MDR compliance efforts, overhead, and risk of divergent quality issues. The tariffs may force firms to weigh these costs against the tariff costs.

Stage 4: Sterilisation

Many medical devices (especially invasive or implantable ones, and sterile disposables) must be sterilised before use. Sterilisation is often outsourced to specialist firms that operate large sterilisation chambers (using Ethylene Oxide gas, gamma radiation, or electron-beam). Key global players have facilities in the U.S., Europe, Mexico, Costa Rica, Malaysia, etc.

Logistically, the typical approach is:

- Devices are assembled (often packaged in a porous pouch that allows sterilant in).

- They are then sent to a sterilisation site (could be in the same factory or nearby, or sometimes in another country if capacity or cost dictates).

- After sterilisation, they might return to the manufacturing site or go straight to packaging/distribution.

Tariffs could come into play if cross-border shipment is needed for sterilisation. For example:

- If a U.S. company manufactures catheters in Costa Rica (a common scenario) and then ships them to the U.S. for ETO sterilisation, previously it was duty-free under CAFTA. Now, unless CAFTA is somehow respected, those catheters entering the U.S. for sterilisation are subject to the 10% tariff (or 25% if they categorize Costa Rica similar to Mexico – though Costa Rica wasn’t explicitly mentioned, presumably it falls under “all imports 10%” since it’s not a targeted country). The company might try to sterilise in Costa Rica instead, but if capacity or quality is an issue, they may have no choice.

- Alternatively, some firms might use Puerto Rico (a U.S. territory) or domestic sterilisation to avoid crossing the border. Puerto Rico, for instance, is a major pharma and medtech manufacturing location specifically because it’s within U.S. customs territory (no import tariff to the mainland).

Sterilisation itself is a service; tariffs apply to goods, not services. But because the goods physically cross a border, they trigger a customs event. One potential workaround some companies could consider is the use of customs bonded zones or temporary import regimes. For instance, the U.S. has provisions for importing goods for processing and re-export without duty (or duty drawback if subsequently exported). If a product is imported solely for sterilisation and then exported, a company might claim a tariff exemption or refund. However, if it’s destined for U.S. sale, that doesn’t help – the tariff will apply on entry as it’s not leaving again.

In Europe, if companies needed to send items across borders for sterilisation, within the EU it’s no problem (single market). If they had to send to, say, the U.S. for gamma sterilisation due to capacity issues, that’s now prohibitive unless absolutely necessary.

Overall, sterilisation is a small but important link. The tariffs encourage firms to perform sterilisation in the same country as assembly or final distribution to avoid extra crossings. The industry may invest in more regional sterilisation capacity as a result (for instance, building an ETO steriliser in Mexico so products can be sterilised before the one-time crossing to the U.S., rather than shipping unsterile products to the U.S. then back out).

Stage 5: Packaging

Packaging is the final step in production – it includes final labelling, boxing, and preparing products for shipment. Often, packaging is done at the manufacturing site right after sterilisation (for sterile goods, the packaging might actually be part of the sterilisation process design). In other cases, bulk products are shipped to a regional distribution center and then packaged or kitted according to local market needs.

For example, a company might manufacture a device in bulk, but country-specific packaging (languages, regulatory info) is added in the destination region. Some medtech multinationals have packaging and kitting centers in places like Belgium or the Netherlands (for EU market) and in the U.S. for the Americas market.

If companies were shipping unpackaged bulk devices across borders for final packaging closer to the customer, tariffs now tax that movement. Thus, we expect more firms will consider packaging at source versus packaging at destination, based on what minimises tariff cost:

- Packaging at source: If a device is assembled in, say, Ireland, the company might fully package and label it for the U.S. in Ireland itself and then ship finished goods. Downside: carrying inventory of many country-specific variants far from the market and less flexibility. Upside: only one border crossing.

- Packaging in market: If parts or unpackaged devices were sent to the U.S. for final packaging, they’d incur tariffs on entry. But then the packaging could be tailored. The value added by packaging is minor, so it likely won’t qualify for changing origin.

Packaging materials (boxes, pouches, trays) themselves might be procured from global suppliers. Tariffs on packaging supplies (plastics, paper) could slightly increase packaging costs too, but that’s a relatively small part of device cost structure.

Stage 6: Distribution and End-Market Delivery

Once devices are made, sterilised, and packaged, they enter the distribution network. This could involve:

- Shipment from factory to regional distribution warehouses.

- Warehousing and inventory management in major markets.

- Shipping to hospitals, clinics, or retailers.

The supply chain might have centralised distribution (e.g., a company uses a single global hub then ships to each country) or decentralised (stock in each region). Tariffs strongly discourage hub-and-spoke distribution that crosses the U.S. border more than once. For instance, some companies used the U.S. as a distribution hub for the Americas – importing products into the U.S., then re-exporting to Latin America. With a 10% tariff on entry and only a possibility to reclaim it on re-export via duty drawback (a cumbersome process), it’s less attractive to route non-U.S. shipments through the U.S. now.

Similarly, European distribution will avoid routing via the U.S. A European company that manufactured in Asia might have previously shipped a batch to its U.S. warehouse and then also supplied some Canadian or Latin American orders from there. With tariffs, they might instead ship directly to those other countries from Asia or set up a distribution center in, say, Panama for Latin America.

From a U.S. healthcare delivery perspective, these supply chain adjustments are mostly behind the scenes, but they could affect lead times and availability. Tariffs inject uncertainty and lead companies to hold more inventory in-market to buffer against supply chain moves (since changing sourcing or routing can cause temporary disruptions). During the initial months of tariff implementation, there is risk of short-term shortages or procurement scramble for certain items, as seen historically when sudden trade barriers occur. The American Hospital Association warned that tariffs on common medical supplies like needles, syringes, and PPE could disrupt the flow of these essentials to providers. For example, many U.S. hospitals rely on cheap import of examination gloves from Malaysia or sterile surgical gloves from Thailand. These now have 10% tariffs (Malaysia/Thailand not specifically high-tariff countries, so baseline 10%). If suppliers increase prices accordingly, hospital procurement budgets are hit; if suppliers try to absorb it, it hits their margins and possibly their ability to supply long-term.

Finally, last-mile distribution (getting devices to the end user) might also see cost increases passed on. Freight, especially air freight, becomes costlier if customs fees rise. Some delicate or time-sensitive devices are air-shipped – adding 10–20% in customs duties on top of that is non-trivial.

In Europe, if the EU retaliates, U.S.-made devices coming into Europe might face tariffs at EU customs. Europe imports a lot of advanced medical devices from the U.S. (imaging equipment, cardiovascular devices, etc.). If, say, the EU imposed a 20% tariff on those in response, European hospitals could see higher prices or supply shifts. MedTech Europe has highlighted that a tit-for-tat trade war involving medical technology between the U.S. and EU would be a “lose-lose scenario for economies and, most importantly, patients”. They emphasise that uninterrupted access is critical and trade barriers will “increase production and distribution costs, delay patient access to critical innovations, and hinder the ability…to remain globally competitive”.

To summarise the supply chain mapping:

- The medtech supply chain is globally distributed at each step, which maximised efficiency under free trade but now creates multiple tariff exposure points.

- Tariffs effectively fragment the chain, pushing companies to do more end-to-end production within one country or trade bloc to avoid multiple duty hits.

- This often means duplicating parts of the chain (e.g., multiple assembly sites for different markets) and losing some efficiency.

The end-market distribution will likely become more regional. Companies will strive to have final goods already within the target market’s borders to avoid last-minute tariffs or delays.

Having mapped these stages, the next section compares the tariff regimes before and after April 2025, to quantify the changes in costs and which materials/products are now caught by tariffs that previously were not.

Previous Tariff Regime vs. New (April 2025) Tariffs

In this section, we provide a comparative analysis of the U.S. trade policy affecting medical devices before the April 2025 announcement versus the new tariff regime. This includes which product categories and materials are impacted and the magnitude of change. Understanding this shift is critical – many business decisions were made under the old rules, and those assumptions have been upended.

U.S. Tariff Regime Before April 2025

General Import Duties: The United States, like the EU and many developed economies, has historically applied low Most-Favored-Nation (MFN) tariff rates on medical devices. As noted, roughly half of medical goods entered tariff-free, and many others carried a nominal duty (2–5%). For example, the U.S. MFN tariff on surgical instruments (HS Code 9018) was 0% in many cases; on patient monitoring devices (HS 9018.19) 0%; on some disposable medical textiles ~7%. There were a few outliers – e.g. certain disposable medical headwear at 6–8% – but by and large, tariffs were not a major cost factor for medtech prior to 2018.

Trade War Tariffs 2018–2021: The Trump administration’s first term saw Section 301 tariffs on Chinese imports. These came in tranches (Lists 1-4) covering about $370 billion of goods. Medical devices and components were caught in some lists, though lobbying won some exclusions. By early 2020, around $5 billion of U.S. medical imports from China were under a 25% tariff. Products hit included imaging equipment parts, some surgical instruments, and consumables like gloves. During the COVID-19 pandemic, many of these tariffs were criticised for hampering access to essential gear. The administration temporarily waived tariffs on certain critical products (77 medical items had exclusions extended through May 31, 2025 under the prior Biden administration). Items like single-use sterile drapes, surgical sponges, diagnostic reagents, and PPE were on that exclusion list – meaning they would have reverted to 25% tariffs in mid-2025 if not extended or if the new regime doesn’t override that.

In addition to China-specific tariffs:

- Section 232 (Steel/Aluminum) Tariffs (2018): 25% on imported steel, 10% on aluminum, globally. The Trump admin imposed these citing national security. The EU, Canada, Mexico initially faced them, then got exemptions or quotas after negotiations in 2019–2021. By 2024, the U.S. had quota deals with the EU (no tariff within quota), and suspended tariffs with Canada/Mexico. Japan still had some quota too. These tariffs indirectly raised the cost of medical device production (steel and aluminum are key inputs for equipment and instruments). For example, U.S. surgical tool makers saw higher domestic steel prices since foreign steel had 25% duty. European steel was not taxed after the 2021 EU-US truce, but now in 2025, the new tariffs may implicitly re-tax EU steel at 20% since that’s a general import, unless the specific 232 quota is still honoured separately (details are complex).

- Other trade disputes: The U.S. and EU had a dispute over aircraft subsidies (Airbus/Boeing) which led to mutual tariffs on various goods in 2019–2020. The U.S. list included some medical devices (for instance, certain syringes or diagnostic equipment from Germany were briefly tariffed ~15% in 2020 as retaliation in that case). However, that dispute was settled with a pause on tariffs in mid-2021.

Summary Pre-2025: By late 2024, the U.S. tariff environment for medtech was:

- Imports from China: generally 25% extra tariff on many devices/components (except those with exemptions).

- Imports from allies (EU, Japan, UK, etc.): largely tariff-free or very low tariff, due to either MFN rates being zero or specific suspensions. Medical technology enjoyed effectively free trade transatlantic in this period.

- NAFTA (Canada/Mexico): duty-free for all medical goods under USMCA, as long as rules of origin are met (which for most devices, they were, given integration).

- Specific categories: Pharmaceutical products (medicines, vaccines) had been explicitly excluded from Section 301 tariffs. Medical devices did not have a blanket exclusion, but some got case-by-case exclusions granted. Pharma in general carried 0% duty under WTO pharmaceutical agreement – something medtech tried to analogously achieve but hadn’t formally.

On the European side pre-2025:

- The EU’s MFN tariff on most medical devices is also low (0–5%). The EU participates in agreements to eliminate duties on many medical items (and some overlap with the Information Technology Agreement for high-tech medical equipment).

- In retaliation to U.S. steel tariffs in 2018, the EU had imposed tariffs on U.S. goods, but they targeted politically sensitive products like motorcycles and bourbon – not medical devices. The EU did prepare a list including medical devices in case the Boeing/Airbus or steel disputes escalated, but as MedTech Europe noted, those were suspended or never implemented fully.

- So EU imports of U.S. medical devices were generally duty-free by 2024, and vice versa.

Cost Structure Under Previous Regime: To illustrate, consider a surgical instrument set imported to the U.S. from Germany in 2024. The base cost $100. Tariff = 0%. Importer’s cost $100, maybe plus a few percent in freight. Now in 2025, that same set has a 20% tariff = $20, so cost $120 – a significant hike.

Another example: nitrile gloves imported from Malaysia in 2024 had an MFN tariff ~2–3%. In mid-2024, Biden’s USTR planned to raise it to 25% by 2026 as part of a broader supply chain review. With Trump’s April 2025 rule, that may have been immediately set to 10% (or perhaps folded into 25% for all goods from Malaysia? Unclear, likely 10%). Already, the trend was upward for some supplies: syringes and needles from China had a 25% tariff and were slated to jump to 50% in Aug 2024 – a massive increase even before the new plan. Such extreme cases show that for certain critical disposable products, costs were on the rise and now layered with more broad tariffs.

New Tariff Regime (April 2025 Onwards)

The new regime can be summarised as:

- Baseline 10% on everything (medical devices, components, raw materials, you name it) coming into the US. If an item was previously 0%, it’s now 10%. If it was previously 5%, now it is 10%. If it was previously under Section 301 at 25%, unclear if that becomes 25+10 or just superseded by 10? In practice, Trump’s plan was described as combining a universal tariff with targeted tariffs. The language suggests the higher nation-specific rates replace the 10% for those countries. But for China, they explicitly said 34% new in addition to previous, totalling 54%. So it appears:

- Countries not on the special list: pay 10%. (This includes likely smaller trade partners, and possibly countries like the UK, Australia, etc., that were not called out.)

- EU: pays 20% (instead of 10%).

- Japan: 24% (instead of 10%).

- China: 54% (this is 10% + 34% new + prior existing 10% (fentanyl) or ? Actually it says base rate 54% before adding Biden or Trump first-term tariffs. This is confusing, but seems they are layering them: earlier tariffs of 25% remain, plus new 34, plus perhaps some specific 20% fentanyl sanction. It could mean some Chinese medical products end up effectively ~79% if all layered – however, for simplicity we use 54% as the “base” for Chinese medtech now, acknowledging it’s drastically high).

- Mexico & Canada: 25% (special case due to other issues). So NAFTA’s free trade is essentially suspended on most goods.

- Others: There was mention in analysis of Vietnam (46%), likely South Korea may also have a rate (perhaps around 20% if considered a “bad actor” on trade balance or something), and possibly others like India could be targeted if deemed reciprocal (India has high tariffs on U.S. medical devices, up to 20% or more, so U.S. might reciprocate similarly).

For medtech specifically, this means:

- All imported medical devices now carry a tariff where many had none. EU imports now 20% (a huge change from 0). Japan imports 24% (also from ~0). These cover a broad swath of devices: imaging machines, diagnostic test equipment, surgical tools, etc.

- Raw materials and components from those regions similarly get those rates. E.g., electronics from Japan now 24%. A magnet for MRI from Japan or EU: 20–24%. Chinese electronic boards: 54%. Even if an item wasn’t previously on a tariff list, now it is at least 10% unless specifically exempted (pharma aside).

- Consumables and accessories: Many of these come from China or Asia. Those from China at 54% essentially price many Chinese suppliers out of the U.S. market unless they cut prices drastically or buyers have no alternative. It’s likely U.S. buyers will turn to other countries for things like basic PPE and disposables. But those other countries still face 10%. So the cheapest source now might be, say, Vietnam or Indonesia at 10% tariff vs China at 54%. We might see a further sourcing shift as a result.

Categories Affected: Unlike previous targeted tariffs that listed specific HS codes (with some medical devices exempted due to public health), the new broad tariffs do not carve out medical technology. Both AdvaMed and the American Hospital Association lamented this fact – industries with humanitarian missions had been exempt in the past, but not this time. So everything from MRI scanners to band-aids is affected. We can highlight:

- Capital Equipment: Imaging (X-ray, MRI, Ultrasound), radiotherapy machines, surgical robots, hospital beds – often imported from the EU or Japan. These now have 20–24% tariffs. Example: A $1 million MRI machine from Germany now costs $1.2 million to import. That $200k either comes out of the hospital’s budget or the manufacturer’s margin or a bit of both. It could tilt purchasing decisions (maybe a U.S.-made competitor like GE Healthcare’s MRI becomes relatively cheaper than a Siemens MRI due to the tariff, influencing hospital choice – a deliberate aim of “Buy American” perhaps).

- Surgical Instruments and Equipment: The EU (Germany) and Pakistan and China are major sources for surgical instruments. Germany and EU: +20%. Pakistan (likely falls under “others 10%”). China: many basic instruments (e.g. scissors, forceps) at 54%. U.S. importers will likely drop Chinese instrument suppliers entirely and switch to Pakistan or India or domestic, even with 10%. Pakistan at 10% now has an advantage over China 54%, but still 10% more expensive than previously.

- Implantable Devices: Many high-end implants (cardiac valves, orthopedic implants) are made in the U.S. and Europe predominantly. If an EU company exports, 20% tariff – e.g., a Swiss implant firm selling in the U.S. will face cost issues. Some implants like orthopedic screws are made in China or India for cost – those are now 54% or 10%, likely shifting sourcing to India (10%).

- Dental equipment and supplies: European dental implants and equipment are now 20% tariffed. This could benefit U.S. dental suppliers at home but might hurt U.S. exports in return if the EU retaliates.

- Diagnostics (IVD) devices and test kits: If imported reagents or analyzers from outside – 10% or more now. Life sciences instruments from Europe get 20%.

- Personal Protective Equipment (PPE): Masks, gloves, gowns – heavily imported. Many of these were tariffed under Section 301, then exempted during COVID. Now, unless those exemptions (77 items) remain in force via extension, they fall under 10%. In fact, the Biden administration had extended most of those healthcare exclusions to May 2025, but it’s unclear if the new Trump tariffs ignore those extensions (likely yes, since his authority is separate). If they lapse, some PPE from China could jump back to 54%. The AHA noted masks and gloves would be 25% by 2024 under Biden’s plan; under Trump’s plan, Chinese masks/gloves might be even higher or at least similar (and non-Chinese at 10%).

- Combination products and others: Some items straddle categories (drug-device combinations, etc.). Pharma drugs stayed exempt, but devices are not. For instance, pre-filled syringes (device + drug) might be considered pharma (exempt) because the drug content – this will get into fine definitions. Generally, pure devices are all included.

Europe vs U.S. Reaction: In the U.S., these tariffs are a unilateral policy – companies have to comply. In Europe, there is the question of retaliation. The EU announced it was “preparing fresh countermeasures”. By mid-April 2025, EU officials talked of a calibrated response, possibly reinstating some tariffs that were previously suspended from the 2018 trade war. MedTech Europe, as cited, is advocating strongly to keep medical devices and inputs off the retaliation list. They point out that the U.S. is both a major supplier and market for EU medtech, so retaliation would hurt European companies and patients too. If their lobbying is successful, the EU might avoid targeting U.S. medical devices (focusing on other sectors like agriculture or consumer goods which are often chosen in trade spats). If not, we could see:

- EU tariff on U.S. medical devices (possibly up to 20% matching the U.S. rate). This would raise costs for European healthcare providers on U.S. products. It could benefit European competitors in the EU market (similar to how U.S. domestic firms benefit in the U.S.), but since many cutting-edge devices are American, it might cause issues for EU healthcare.

- Tit-for-tat escalation: The U.S. could then conceivably raise tariffs further, etc., though given they’ve already blanketed everything, further escalation tools are limited (short of quotas or bans).

Special Cases – Distributed Production: The new tariffs also handle unusual cases. For instance, if a device is produced in multiple countries, the final tariff depends on the “country of origin” as per customs rules (usually where the last substantial transformation happened). Some firms could try to shift the final substantial transformation to a low-tariff country. For example, an EU-made device shipped to, say, Singapore for a minor transformation and then to the U.S. might legally become Singapore-origin, thus only 10%. However, customs authorities are strict on such rule-of-origin gaming. Also, the cost and complexity might not be worth it unless for very high value items.

Currency and other factors: It’s worth noting that currency fluctuations or pricing strategies can sometimes offset tariff impacts. E.g., if the Euro weakened significantly against the dollar, European exporters might naturally become cheaper, offsetting some of the tariff. But currency is volatile and not something companies can rely on. Trade strategies will focus on supply chain changes more.

In conclusion, the new tariff regime is both broader and higher:

- It sweeps in categories of medtech products that never before incurred tariffs, essentially taxing the entire sector for the first time at scale.

- It dramatically increases the tariff rate on products that were already tariffed (e.g., from 25% to 54% for China, or from 0% to 20% for EU).

- It affects raw materials, components, and finished goods alike, thereby compounding costs if a product crosses borders multiple times in its lifecycle.

- By comparing before vs after, we see that a global supply chain that might have had zero tariffs end-to-end (e.g., EU components -> Mexico assembly -> US market under USMCA had no duties) could now face multiple tariffs (EU to MX 0%, but MX to US 25%; or EU direct to US 20%). This is a fundamental change in cost structure.

Next, we turn our attention to how these tariff changes impact companies in practical terms – examining U.S. vs European companies, and differences between large multinationals and smaller firms.

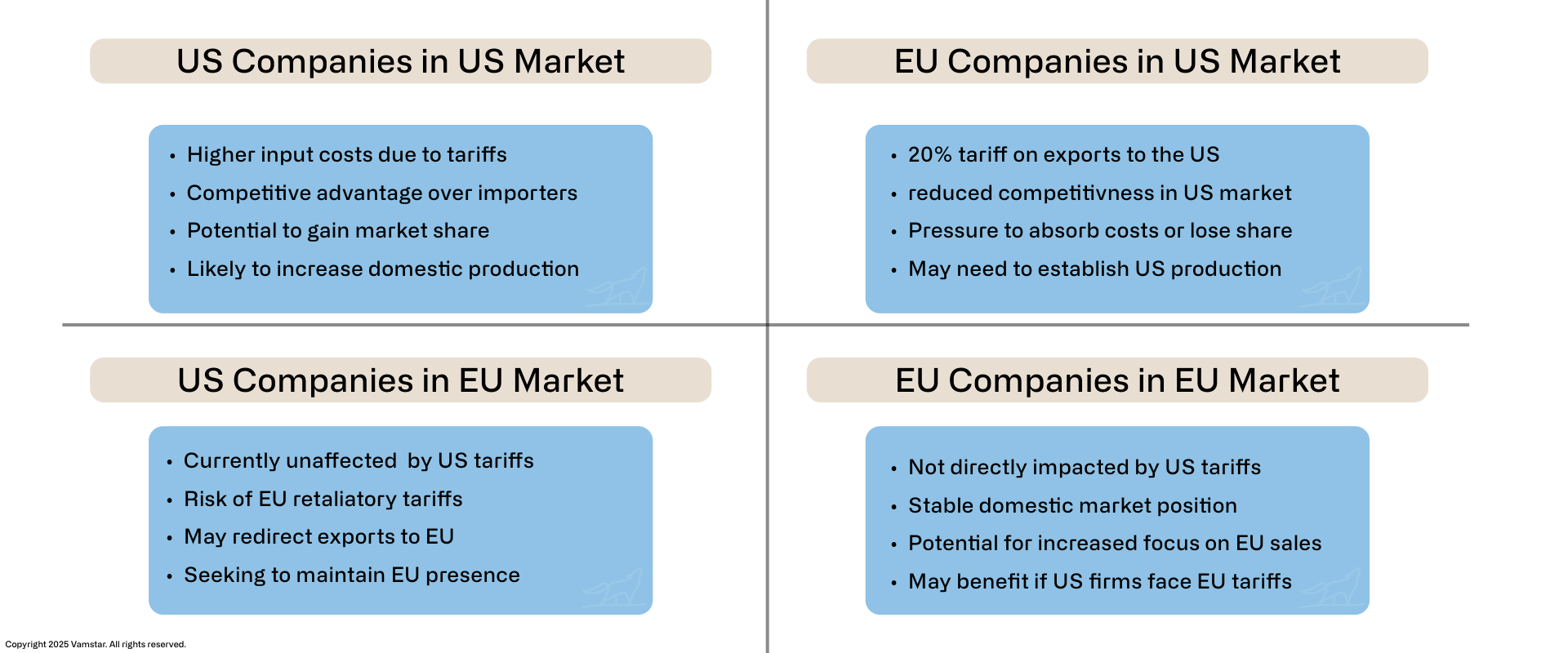

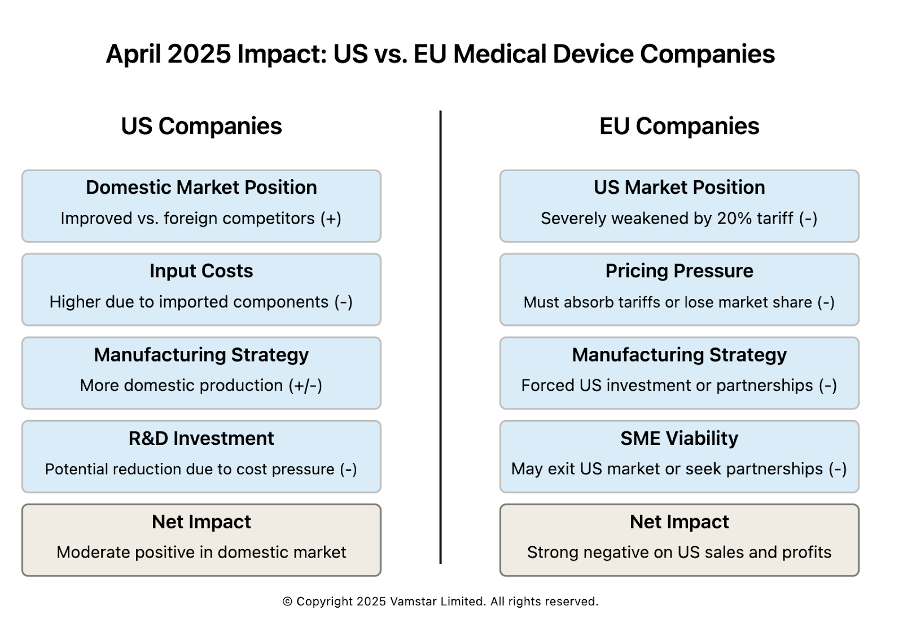

Impact on U.S. vs. European Medical Device Companies

Figure 4: US vs EU Medical Device Companies

Both U.S. and European medical device companies are being forced to adapt, but the nature of the impact differs given their typical supply chain orientations and market dependencies. We will analyse each in turn, noting common challenges and unique advantages or disadvantages.

Impact on U.S. Medical Device Companies

The United States hosts many of the world’s largest medical device manufacturers (e.g. Medtronic, Johnson & Johnson’s DePuy Synthes, Abbott, GE Healthcare, Stryker, Becton Dickinson) as well as countless midsize and niche firms. Key impacts on these companies include:

- Higher Input Costs for U.S. Manufacturers: Even companies manufacturing in the U.S. often rely on imported inputs (specialised components, raw materials). With the blanket tariffs, their cost of materials goes up. For instance, a Minnesota-based pacemaker factory might import circuit boards from China (now +54%) or capacitors from Japan (+24%). While some critical medical components from China had been excluded from tariffs for a while, those exclusions may not continue. As one supply chain expert noted, medtech companies “may be producing devices in the U.S. but sourcing raw materials and assemblies from other countries” – meaning tariffs hit their supply chain. The immediate result is squeezed gross margins unless mitigated.

- Competitive Position in U.S. Market: U.S. companies selling domestically gain a relative advantage over foreign importers to the U.S., since those imports now carry tariffs. For example, a U.S.-made hip implant competes with a German-made implant in the U.S.; the German one now faces +20% duty, effectively making the U.S. one comparatively cheaper (even if the U.S. firm has some higher input cost, it’s likely less than 20%). This could boost sales or allow U.S. firms to increase prices a bit, capturing more profit, if customers shift to domestic products to avoid tariffs. This advantage will be most pronounced in product categories where there are both strong U.S. and foreign suppliers. In categories dominated by imports (e.g. some surgical instruments from Germany/Pakistan or disposable supplies from China/Malaysia), the U.S. doesn’t automatically get an alternative source, so the advantage is moot and it just means all buyers pay more. But where an alternative exists, U.S. firms will highlight their “Made in USA” status.

- Exports and Foreign Sales: Many U.S. companies also export devices worldwide, including to Europe and Asia. If the trade war prompts retaliation, U.S. companies could face tariffs abroad, hurting their sales. Right now, European tariffs on U.S. medtech are a risk but not yet a reality (pending EU response). Beyond tariffs, another concern is if foreign governments favour local suppliers in response (economic nationalism). For instance, China might fast-track its efforts to source medical equipment domestically or from non-U.S. countries due to the hostile U.S. trade stance (China was already doing this for high-tech medical gear in recent years). So U.S. multinationals might see a tougher environment in China (which is a growing market for medtech) on top of tariffs. Europe is less likely to shun U.S. tech given fewer alternatives in some areas, but if EU imposes duties, U.S. products become pricier for European hospitals, potentially reducing sales or margins in that market.

- Supply Chain Reconfiguration: U.S. companies are actively diversifying supply chains in response. Even before these tariffs, trade tensions had spurred diversification away from China. Now, with tariffs hitting essentially everywhere, the strategy is shifting to localisation. U.S. firms are considering moving more production onshore. However, as Harvard Business School’s Willy Shih noted, “We live in an interdependent world, and if we want to break those interdependencies, it is not going to happen overnight”. In the short term, U.S. companies might rely on stockpiling (in fact, some rushed shipments in Q1 2025 ahead of tariff implementation – similar to how pharmaceutical companies expedited shipments before tariffs). Longer term, they might invest in domestic capacity or in countries with trade agreements. But with the U.S. essentially taxing all countries, the only safe haven is domestic (or maybe a free trade zone if they can creatively use it). One immediate effect is increased demand for domestic suppliers – which could drive up their prices too due to demand, ironically.

- R&D and Investment Impact: AdvaMed’s CEO warned that broad tariffs would cause companies to cut R&D spending first. U.S. medtech leads the world in innovation partly because strong profits fund high R&D (industry average ~8–10% of sales goes to R&D in medtech). If margins shrink due to tariffs, companies may curtail R&D investment in new products, hurting future competitiveness. They might also delay capital investments or hiring. In a Morningstar analysis, it was noted that facing these tariffs, producers might suffer lower margins and there’s “no room for error” now on cost control. Some firms may shift investment to automation or commercial efficiency to counteract cost increases.

- SMEs vs. Large Players: Small and mid-sized U.S. medtech companies are often less diversified in manufacturing and sourcing. If an SME imports one critical component and its cost goes up 20%, that could erase their profit on the final device if they can’t raise the price. Large companies can sometimes negotiate with suppliers to share the burden or redesign products to use alternate parts. SMEs have less negotiating power and less bandwidth for engineering changes. Also, big companies can absorb short-term margin hits more easily or hedge currency/commodity costs. SMEs might face immediate financial stress. One possible outcome is consolidation – SMEs unable to cope may seek acquisition by larger firms that can restructure the supply chain. We might also see SMEs lobbying via associations (like how many joined AdvaMed’s call for exemptions).

- Mitigation Tactics: U.S. companies are exploring mitigation: applying for exclusions (the administration could allow certain critical devices to be exempt on a case-by-case basis), utilising Foreign Trade Zones (FTZs) to defer tariffs on imported components until the product leaves the zone – potentially exporting from the zone without ever paying U.S. tariff if the product is exported. There’s also the “first sale” rule (re-valuing goods for customs at an earlier sale price if multi-tier). However, these are technical and not always applicable. By and large, medtech firms have limited tariff mitigation avenues compared to, say, the consumer electronics industry. Ultimately, raising prices is a direct mitigation (passing cost to customer), but in healthcare that can have public relations and demand consequences.

In summary for U.S. companies: They face higher costs and uncertainty in the short term, but potentially improved competitiveness at home vis-à-vis imports. The net effect depends on their import reliance vs export reliance. A company like Stryker (which manufactures a lot in the U.S. and sells in U.S.) might net benefit relative to foreign competitors, whereas a company like, say, Zimmer Biomet (if hypothetically it sourced many parts from abroad for U.S. assembly) might see more pain. Many big firms do both – import some, export some – creating a mix of effects.

Notably, the U.S. medtech industry is pushing for policy adjustments. AdvaMed is in talks with the White House to explain the importance of medtech and request exemption. The American Hospital Association is highlighting how these costs ultimately burden healthcare providers and patients. Whether those pleas will yield carve-outs is uncertain; so far the administration’s stance seems firm on across-the-board tariffs.

Impact on European Medical Device Companies

Europe is home to leading medtech companies as well (Siemens Healthineers, Philips, Roche Diagnostics, Fresenius, Smith & Nephew, Dräger, to name a few across various countries) in addition to a vibrant ecosystem of specialized SMEs, especially in Germany, Switzerland, and the UK. The U.S. tariff policy directly affects European firms mainly in their role as exporters to the U.S. and as participants in global supply networks. Key impacts:

- Loss of Price Competitiveness in U.S. Market: Europe exports a large volume of medical devices to the U.S. – the trade is substantial (the U.S. is Europe’s #1 medtech export destination). A 20% tariff on these exports is a big blow. European firms essentially have three choices: absorb the cost (reducing their margins), pass it to U.S. customers (risking reduced sales), or find a way to avoid the tariff (e.g., produce in the U.S.). In the short run, many will likely have to absorb at least part of it because hospitals often have contracts or budgets set in advance. This directly hits profit. For example, Philips (Netherlands) selling imaging equipment to U.S. hospitals will find its products effectively 20% more expensive overnight. To maintain volume, Philips might have to discount its prices by, say, 10% and let the other 10% be passed on, sharing the pain with buyers. Even then, a competing U.S. vendor can swoop in saying “no tariff on ours,” possibly taking market share.

- Pressure to Invest in U.S. Manufacturing: Many European firms are now evaluating production in the U.S. If the U.S. market is large enough, building or expanding a U.S. plant may pay off to circumvent the tariff. Companies like Siemens Healthineers already make some products in the U.S. (they have facilities for laboratory diagnostics and imaging assembly in the U.S.). They could ramp those up or introduce new production lines. However, building manufacturing capacity is capital-intensive and slow. In the interim, some may resort to contract manufacturing in the U.S. – essentially hiring a third-party manufacturer state-side to assemble their products under license. This has IP and quality control considerations, but for simpler products it could be viable.

- SMEs Face Barriers: European SMEs that export to the U.S. are in a particularly tough spot. They likely don’t have a U.S. presence to shift production to, and their export volumes might not justify setting one up. For instance, a small German company making a specialized diagnostic device that sells, say, $5 million a year in the U.S. now sees a 20% tariff ($1M cost). That might wipe out their profit from the U.S. sales entirely. They might choose to pull out of the U.S. market or find a U.S. distributor who’s willing to perhaps assemble final kits in the U.S. to lower duties. Alternatively, if they sell via distributors in the U.S., those distributors may demand price cuts to offset the tariff, again hitting the SME’s margins. It could lead to some niche European products disappearing from the U.S. market, at least temporarily, which can ironically reduce competition and choice in the U.S. (contrary to what one might want in healthcare).

- Home Market (Europe) Impacts: While the U.S. tariffs don’t directly impose costs on European domestic operations, there are indirect effects. If U.S. competitors become relatively stronger (due to protective effects in the U.S.), they could funnel more resources into Europe. Also, if the EU and U.S. get into a tit-for-tat, European firms could get hit by U.S. retaliation beyond tariffs (in worst-case scenarios, regulatory hurdles or procurement preferences for U.S. could emerge). But sticking to tariffs: should the EU retaliate and include medtech, then European companies would suffer from higher costs on imported U.S. components (some European devices use U.S.-made components like certain high-end electronics or materials). MedTech Europe’s statement clearly indicates European firms worry that tariffs on inputs will “hinder…domestic industries’ ability to achieve efficiencies, foster innovation” and ultimately “burden healthcare systems” with cost. They frame it as harming both businesses and patients – a compelling argument to exclude medtech from any EU tariff list.

- Supply Chain Adaptation: European companies, much like U.S. ones, will try to adapt their supply chain. For goods destined to the U.S., one adaptation might be routing through other countries or final assembly elsewhere, as discussed. For example, a European firm might consider doing final assembly in Mexico (which now is unfortunately 25% – so not helpful) or Canada (25% as well – also hit). Perhaps in a country like Costa Rica (10%) or Malaysia (10%) that has lower tariffs. However, then the product is “Made in Costa Rica” and gets 10% into the U.S. – better than 20%. But moving a production line to Costa Rica or Southeast Asia is not trivial either and usually done for cost reasons, not tariff. If it’s a high margin device, absorbing 20% might be less painful than moving the whole supply chain. Thus, many European firms may initially accept reduced U.S. profitability while watching policy developments.

- Market Strategy and Pricing: Some European firms might strategically focus more on other markets if the U.S. becomes too costly to serve. The EU, Middle East, Asia could get more attention. However, the U.S. is the world’s largest medtech market (~40% of global sales), so it’s hard to ignore. More likely, European companies will re-double lobbying via diplomatic channels. The coordinated push by trade associations on both sides (AdvaMed and MedTech Europe) suggests a united front urging that medical technology be spared in future adjustments. If any sector might get relief for humanitarian reasons, it could be this – but there’s no guarantee.

- Financial and Operational Strain: European multinationals often have global supply chains similar to U.S. ones. A company like Medtronic (though nominally Irish, it has huge operations in both the U.S. and EU) will see internal complexities. But focusing on EU-headquartered ones: they have to explain to shareholders that a significant tariff is hitting their U.S. sales. Stock prices of some European medtech firms could drop due to expected margin compression. They’ll likely announce cost-saving initiatives to counteract (often code for some combination of layoffs, sourcing changes, and commercial efficiency drives).

One interesting angle: some European firms might consider partnerships with U.S. companies to get around issues. For example, an EU SME might license its product to a U.S. company to manufacture and sell in the U.S., rather than exporting it. This way the product still reaches the market but via a U.S. partner (avoiding tariffs as domestic production). The downside is the European SME loses some control and profit share. But it could be a stopgap measure – essentially tech transfer in exchange for market access.

- Long-term Competitiveness: If tariffs persist long-term, European companies might lose market share in the U.S. which can be hard to regain. The U.S. healthcare system might “lock in” domestic alternatives or shift to others. This could diminish European firms’ global scale, which in turn can raise their unit costs (as they produce less volume) and reduce R&D budgets. It’s a dangerous cycle. Conversely, if they manage to invest and produce in the U.S., they effectively become local players for that market, which might be the new normal – but with duplication of effort and loss of synergy.

European companies do have the EU market as a relatively safe base still open – unless they face U.S. competition there aided by no EU response. If the EU doesn’t retaliate on medtech, ironically U.S. companies could still export to Europe tariff-free, giving U.S. firms an advantage in Europe (cheaper than EU firms’ products which face U.S. tariffs). That scenario is asymmetric: EU firms get hit in the U.S., U.S. firms not hit in the EU. European industry would find that very unfair. Politically, the EU might then feel compelled to do something to level it. MedTech Europe’s stance is to avoid patient harm by keeping trade open both ways, which is ideal in principle, but may not be tenable in a prolonged dispute. The EU Commission might negotiate with the U.S. for removal of medtech tariffs mutually. If not, they might at least threaten reciprocal tariffs on medtech to force a carve-out.

In summary, European medtech companies face strong headwinds in their most important export market, the U.S. They will likely see reduced profits and possibly market share in the U.S. unless they adapt by localising production or lowering prices. The uncertainty of trade relations also makes planning difficult – as one expert said, “Until we figure out what sticks, we face a lot of uncertainty, and uncertainty means additional cost”. European firms, especially SMEs, may need support (perhaps government export aid or tax relief) to weather the storm if the situation drags on.

Having looked at U.S. vs European companies broadly, the next section will explore concrete scenarios of how a company with facilities in multiple regions might manage the tariffs, and how tariffs apply depending on various origin-destination combinations. This will illustrate some strategic decisions companies are considering.

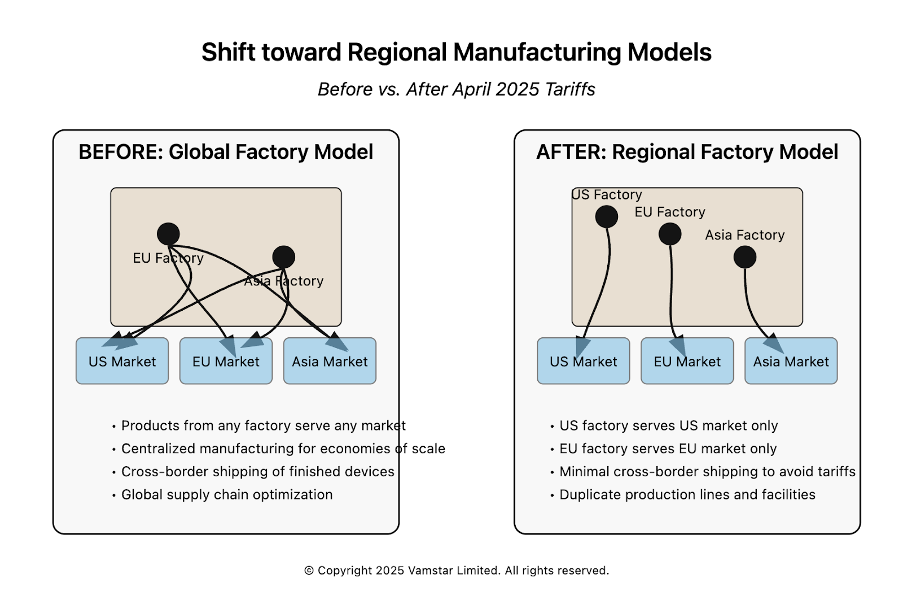

Scenario Analysis: Distributed Manufacturing Footprints and Tariff Application

Figure 5: Manufacturing Models and their Re-alignment

Many medium and large medical device companies operate in multiple countries. They might have R&D in one country, component manufacturing in another, final assembly in a third, and sales globally. Such distributed manufacturing footprints were designed for efficiency, resilience, and local market access. The new tariff environment forces these companies to rethink how they allocate production. In this section, we will consider a few representative scenarios and examine how tariffs apply and what strategic choices the company could make in each.

Scenario 1: U.S. and European dual manufacturing (Regionalisation)

Company A is a multinational that manufactures a particular medical device (say a complex diagnostic machine) in two locations – the U.S. and Germany. Before tariffs, it might have been splitting production: the German plant served worldwide orders including the U.S., and the U.S. plant served mostly North America but also exported some to Asia. Both plants imported some parts from Asia (circuit boards, etc.).

- Pre-2025: No U.S. tariffs on German-made finished devices, so it didn’t matter that some U.S. sales came from Germany. The company could balance load between plants optimally. Let’s say 50% of U.S. demand was fulfilled from Germany, 50% from U.S. Now, those German imports get hit 20%.

- Post-2025: Company A will likely decide to serve the U.S. market exclusively from its U.S. plant to avoid the 20% on finished goods. The German plant might then focus on Europe and other regions. This means an operational re-jig: more production volume in the U.S. (possibly overtime or capacity expansion) and less in Germany (maybe freeing capacity to export more to Asia or to fill in if Asian suppliers falter). Tariffs on components: If the German plant was sending sub-assemblies to the U.S., they now incur 20% too, so better to send just raw components from Asia to both plants separately rather than sub-assemblies between EU/U.S. The company might also redirect component sourcing: e.g., if they used a German-made widget in all machines, perhaps now the U.S. plant will source that widget from a U.S. supplier or a “neutral” country supplier to avoid the 20% on importing it from Germany. In other words, intra-company trade between the U.S. and EU will be minimized. Each plant will try to be as self-sufficient as possible for its region.

Outcome: The company avoids finished goods tariffs into the U.S., but at cost of some duplication. The German plant might face higher unit costs (lower volume) and perhaps consider scaling down or repurposing. The U.S. plant might invest in capacity (good for U.S. jobs in the short term). The overall company supply chain becomes less flexible – capacity can’t be easily shifted across the Atlantic to handle surges, because doing so would incur tariffs.

If the EU retaliated symmetrically (20% on U.S.-made devices into the EU), Company A might also ensure the EU market is served only from Germany. Which it already does mostly, but any small exports from the U.S. to EU would stop. Essentially, each market becomes an island for final assembly.

Scenario 2: U.S. company with low-cost country manufacturing (Offshoring vs Onshoring)

Company B is a U.S.-headquartered firm that makes a high-volume disposable medical product, e.g. blood glucose test strips. It set up a factory in Malaysia years ago to leverage lower costs, exporting all strips to the U.S. (and worldwide) from Malaysia. Under the new tariffs, Malaysia isn’t a targeted country so it faces the 10% baseline U.S. tariff.

Options:

- Keep status quo: Continue making in Malaysia, accept 10% tariff on import. This will increase cost per strip. Company B can try to pass some of that to distributors or consumers (noting that these are often reimbursed products, pricing can be sensitive). 10% might be manageable, especially if Malaysia’s cost base is, say, 30% cheaper than U.S. manufacturing. They’d lose some cost advantage but not all.

- Shift assembly to the U.S.: They could build an automated production line in the U.S. (since labour is a big part of cost, automation would be key). This avoids tariffs but could raise production costs by more than 10%. If U.S. production is, say, 20% more expensive than Malaysia even after tariff, it’s not worth shifting. They might try a hybrid: keep raw strip production in Malaysia, then import semi-finished strips in bulk and do final packaging in U.S. to attempt to claim a different tariff treatment. But likely the tariff still applies on import of strips as the main component.

For Company B, 10% might not justify a drastic move yet, especially if they anticipate these tariffs might be temporary or negotiable. If tariffs rose higher or if Malaysia got targeted (imagine an expanded list of “bad actors”), then they’d reconsider.

Notably, if Company B also sells globally, it might try to designate the Malaysia plant to serve all non-U.S. markets, and perhaps open a small U.S. line just for domestic needs. This is the regional strategy again, but depends on scale.

- Alternate sourcing: If Company B’s Malaysia plant imports raw materials (maybe enzymes for the test strips from the U.S.), could they move that to a different source? If the U.S. is an input supplier, Malaysia might put retaliatory tariffs (but Malaysia is unlikely to retaliate independently; it might benefit from companies shifting sourcing to it since it’s only 10%). So Company B might actually source more from Malaysia or similar 10% countries and less from China (54%) for any inputs.

Scenario 3: European SME exporting to U.S. (Market Exit vs U.S. Partnership)

Company C is a UK-based SME that produces a specialised neurology diagnostic device, selling to a few U.S. clinics and distributors. It exports ~100 units a year to the U.S. at $50k each (so $5 million revenue). They manufacture entirely in the UK.

- Tariff impact: 20% on entry means an extra $10k per device in customs duty. This either makes their device $60k for buyers or forces them to drop their price or margin by $10k. As a small company, $5m might be a large chunk of their revenue. $10k less per unit is a $1m total hit, which could wipe out their profit since SMEs often have maybe 10-20% profit margin.

- Choices:

- Absorb it and operate at break-even or loss in the U.S. – not sustainable long term.

- Raise U.S. price to $60k – will U.S. clinics pay 20% more? Possibly not if there are alternatives or tight budgets. They might lose customers, which might drop revenue even more.

- Partner/License: They could approach a U.S. medical device company and license the design or establish a contract manufacturing deal in the U.S. The U.S. partner could assemble the device (maybe the UK company ships some components or provides know-how). The devices then count as U.S.-made. Company C then gets maybe a royalty or some fee arrangement. This sacrifices some margin but might keep the product available in the U.S. without tariff. The downside is complexity of finding the right partner and potential IP risks.

- Exit the U.S.: Focus on the UK, Europe and other markets. If those markets suffice for viability, they might temporarily pause U.S. sales. This is a loss for U.S. patients who liked that specialised device. It also reduces Company C’s growth potential.

This scenario underscores how SMEs, with fewer options, might either innovate in business models (partnerships) or retrench geographically. It also shows how tariffs can reduce competition: if Company C exits, maybe a larger competitor (possibly U.S.-based) picks up its customers, resulting in less choice or higher prices.

Scenario 4: Multinational with a Complex Global Supply Chain (Re-optimising flows)

Company D is a large multinational (perhaps based in the U.S.) that has truly globalised its supply chain: It has a design center in California, component plants in China and Mexico, final assembly in Ireland for some product lines and in Puerto Rico for others, and distribution centers in Belgium and in Tennessee.

This kind of network is not unusual for top 10 medtech companies. Under tariffs:

- China components to Ireland: previously 25%, now effectively at least 54%. If those components can instead be made in, say, Thailand or sourced from Mexico, that’s 10% or 25%. Company D might expedite supplier qualification in other countries for parts currently coming from China (a trend already underway).